For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. He is the sole author of all the materials on AccountingCoach.com.

For 25 years I observed college students struggling with the bookkeeping and accounting terms “debit” and “credit”. They easily memorized that asset accounts should normally have debit balances, and those debit balances will increase with a debit entry and will decrease with a credit entry. They also memorized that liability and owner’s (or stockholders’) equity accounts normally have credit balances that increase with a credit entry and decrease with a debit entry. It was easy to accept that every transaction will affect a minimum of two accounts and that every transaction’s debit amounts must be equal to the credit amounts.

Things got a little shaky when they were told to credit a revenue account when a company has earned fees or sold products. (After all, they had memorized that credits reduce asset account balances and increase the credit balances in the liability accounts.) A similar problem occurred when they were told to debit an expense account when a company incurs an expense. (After all, a debit increases the balance in an asset account and decreases the credit balance in a liability account.)

After reviewing the feedback we received from our Explanation of Debits and Credits, I decided to prepare this Additional Explanation of Debits and Credits. In it I use the accounting equation (which is also the format of the balance sheet) to provide the reasoning why accountants credit revenue accounts and debit expense accounts.

Hopefully this will give you a deeper understanding of the terms debit and credit which are central to the 500-year-old, double-entry accounting and bookkeeping system. Since this system is included in today’s accounting software, the better you understand it the more confident and effective you will be in your tasks and in your communication with superiors, peers, clients, and others you want to help.

WATCH NOWAdvance Your Career with Our PRO Training

Please let us know how we can improve this explanation

No Thanks

Close

Pertinent Facts Relating to Debits and Credits

To get started, let’s review some facts that you should already be aware of as a bookkeeper, accountant, small business owner, or student.

Debits, Credits, Double-Entry, Accounts

Debit means left side. Its abbreviation is dr. (Apparently the Italian or Latin word from which debit was derived included an “r”). Do not think of debit as good, bad, or anything else.

Credit means right side. Its abbreviation is cr. Do not think of credit as good, bad, or anything else.

Double-entry means an accounting system in which every transaction is recorded with amounts entered in two or more accounts. Further, the amounts entered as debits must be equal to the amounts entered as credits. If this is done for every transaction and without errors, then all the amounts appearing in the accounts will have the total amount of debits equal to the total amount of credits.

Accounts are the bookkeeping or accounting records used to sort and store a company’s transactions. Some of the accounts will have titles such as Cash, Accounts Receivable, Inventory, Equipment, Accounts Payable, Common Stock, Sales, Wages Expense, Rent Expense, Interest Expense, and perhaps hundreds more. The accounts can be found in the company’s general ledger. Hence, these accounts are also known as general ledger accounts.

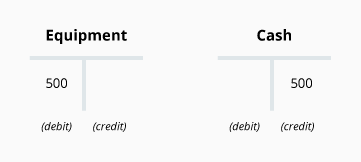

T-accounts are a sketch or visual aid (outside of the general ledger) that are used by accountants in order to see the effects of the debit and credit components of a transaction. The left-side of the “T” is used for the debit amounts, while the right side is used for the credit amounts. Hence, if a company pays $500 for equipment, the two relevant T-accounts will look like this:

The accounts are usually arranged in the general ledger according to the following classifications:

Assets

Liabilities

Owner’s (stockholders’) equity

Revenues

Expenses

Gains

Losses

The balance sheet accounts consist of these account classifications:

Assets

Liabilities

Owner’s (stockholders’) equity

The income statement accounts consist of these account classifications:

Revenues

Expenses

Gains

Losses

Formats of the Balance Sheet and Accounting Equation

One of the main financial statements is the balance sheet (also known as the statement of financial position).

The format of the balance sheet for a sole proprietorship is:

The format of the balance sheet for a corporation is:

The format of the accounting equation (or basic accounting equation or bookkeeping equation) is identical to the format of the balance sheet.

Balance Sheet Accounts are Permanent Accounts

A company’s general ledger accounts can also be viewed as one of two types:

permanent accounts

temporary accounts

The permanent accounts are the balance sheet accounts. In other words, the permanent accounts are the accounts used to record and store a company’s amounts from transactions involving assets, liabilities, and owner’s (stockholders’) equity.

The balance sheet accounts are referred to as permanent because their end-of-year balances will be carried forward to the next accounting year. The permanent accounts are sometimes described as real accounts.

Recap: The asset, liability and owner’s (stockholders’) equity accounts are known as balance sheet accounts, permanent accounts, and real accounts.

Income Statement Accounts are Temporary Accounts

The general ledger accounts that are not permanent accounts are referred to as temporary accounts.

Temporary accounts are generally the income statement accounts. In other words, the temporary accounts are the accounts used for recording and storing a company’s revenues, expenses, gains, and losses for the current accounting year.

The income statement accounts are temporary because their balances are not carried forward to the next accounting year. Instead, the balances in the income statement accounts will be transferred to a permanent owner’s equity account or stockholders’ equity account. After the transfer, the temporary accounts are said to have “been closed” and will then have zero balances.

By starting each year with zero balances, the income statement accounts will be accumulating and reporting only the company’s revenues, expenses, gains, and losses occurring during the new year.

Recap: The revenue, expense, gain, and loss accounts are known as income statement accounts, temporary accounts, and are sometimes known as nominal accounts.

After the Temporary Accounts are Closed

Immediately after the temporary accounts are closed by transferring their balances to an owner’s equity or stockholders’ equity account, the only accounts with non-zero balances will be the permanent accounts.

With the balances from the temporary accounts now included in the permanent accounts, the balance sheet and the accounting equation can be prepared in the following format:

or

The Income Statement Accounts Have an Immediate Effect on Owner’s Equity or Stockholders’ Equity

Even though we do not record revenues, expenses, gains and/or losses directly into an owner’s equity account (or stockholders’ equity account) when we record the transaction, you must realize that owner’s equity or stockholders’ equity is also increasing or decreasing.

For example, at the time that a company earns and receives $500 of cash from providing a consulting service, the company’s assets increase by $500 and its owner’s equity or stockholders’ equity increases by $500. This is occurring even though the transaction is recorded with an entry to Cash (a permanent asset account) and an entry to Consulting Revenues (a temporary account). Again, you need to understand that the $500 credit entry to Consulting Revenues is causing a $500 increase in a permanent account that is part of owner’s equity or stockholders’ equity.

We will continue this discussion later, but for now take note that a credit entry is required to increase owner’s equity or stockholders’ equity.

Please let us know how we can improve this explanation

No Thanks

Close

Normal Debit and Credit Balances for the Accounts

We will now return to the format of the balance sheet and the basic accounting equation:

The format of the basic accounting equation can help you understand the normal or expected balances for the general ledger accounts. It will also assist you in understanding the type of entry required to increase an account balance. Here are the relevant points:

Asset accounts normally have debit balances and the debit balances are increased with a debit entry.

Remember that debit means left side.

In the accounting equation, assets appear on the left side of the equal sign.

In the asset accounts, the account balances are normally on the left side or debit side of the account.

Therefore, the debit balances in the asset accounts will be increased with a debit entry.

Liability accounts will normally have credit balances and the credit balances are increased with a credit entry.

Recall that credit means right side.

In the accounting equation, liabilities appear on the right side of the equal sign.

In the liability accounts, the account balances are normally on the right side or credit side of the account.

Therefore, the credit balances in the liability accounts will be increased with a credit entry.

The owner’s capital account (and the stockholders’ retained earnings account) will normally have credit balances and the credit balances are increased with a credit entry.

Again, credit means right side.

In the accounting equation, owner’s (stockholders’) equity appears on the right side of the equal sign.

In the owner’s capital account and in the stockholders’ equity accounts, the balances are normally on the right side or credit side of the accounts.

Therefore, the credit balances in the owner’s capital account and in the retained earnings account will be increased with a credit entry.

Please let us know how we can improve this explanation

No Thanks

Close

Examples of Debits and Credits in a Sole Proprietorship

Let’s reinforce our debit and credit discussion by using five examples. In this section we will assume that the business is a sole proprietorship. (After these examples, we will illustrate the debit and credit entries for a corporation.)

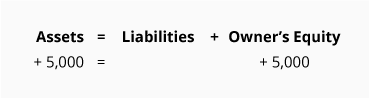

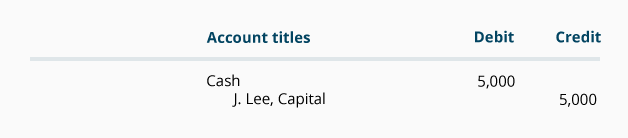

J. Lee starts a sole proprietorship with $5,000 of her own money

When J. Lee invests $5,000 of her personal cash in her new business, the business assets increase by $5,000 and the owner’s equity increases by $5,000. As a result, the accounting equation for the business will be in balance.

Since assets are on the left side of the accounting equation, the asset account Cash is expected to have a debit balance. The debit balance in the Cash account will increase with a debit entry to Cash for $5,000.

The other part of the entry will involve the owner’s capital account (J. Lee, Capital), which is part of owner’s equity. Since owner’s equity is on the right side of the accounting equation, the owner’s capital account is expected to have a credit balance and will increase with a credit entry of $5,000.

The transaction in the general journal form is:

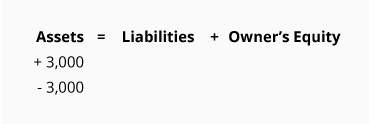

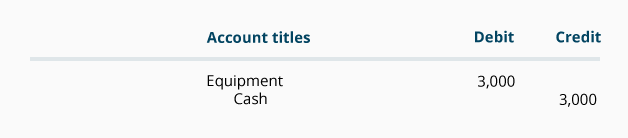

The business purchases equipment for $3,000

When the business pays $3,000 of its cash for new equipment, the business asset account Cash decreases by $3,000 and the business asset account Equipment increases by $3,000. The following shows that this transaction will keep the accounting equation totals and the balance sheet totals in balance:

Note: In this topic we show only the change in the accounting equation. To see the cumulative amounts for multiple transactions, visit our Accounting Equation Explanation.

Since assets are on the left side of the accounting equation, the asset account Equipment is expected to have a debit balance. Since the Equipment account is increasing by $3,000, a debit entry to Equipment for $3,000 is needed.

The other part of the entry will involve the asset account Cash, which is expected to have a debit balance. Since the Cash account is decreasing by $3,000, the Cash account must be credited for $3,000.

The transaction in the general journal form is:

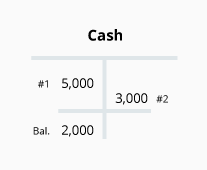

The following T-account illustrates how the debit and credit amounts from the first two transactions have affected the Cash account:

Since Cash is an asset account, its normal or expected balance will be a debit balance. Therefore, the Cash account is debited to increase its balance. In the first transaction, the company increased its Cash balance when the owner invested $5,000 of her personal money in the business. (See #1 in the T-account above.) In our second transaction, the business spent $3,000 of its cash to purchase equipment. Hence, item #2 in the T-account was a credit of $3,000 in order to reduce the account balance from $5,000 down to $2,000.

Note that the T-account is usually a sketch the accountant or bookkeeper makes in order to visualize the effects that a transaction will have on the two or more accounts involved in a transaction. (The account appearing in the company’s general ledger will NOT be in the form of a “T” as we show it here.)

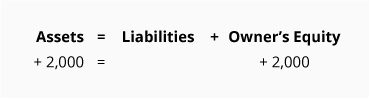

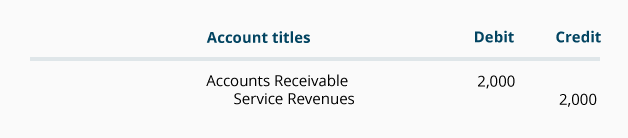

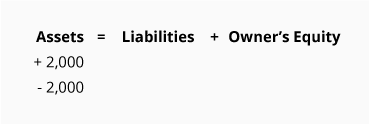

The business earns service revenues of $2,000 and allows the customer to pay 10 days later

When the business earns $2,000 by providing a customer with services, the business assets increase by $2,000 and the owner’s equity increases by $2,000. The change in the accounting equation will be:

Since assets are on the left side of the accounting equation, the asset account Accounts Receivable is expected to have a debit balance. The debit balance in Accounts Receivable is increased with a debit to Accounts Receivable for $2,000.

The other part of the entry involves the owner’s capital account, which is part of the owner’s equity. Since owner’s equity is on the right side of the accounting equation, the owner’s capital account (which is expected to have a credit balance) is increased with a credit entry of $2,000. However, instead of recording a credit entry directly in the owner’s capital account, the credit entry is recorded in the temporary income statement account entitled Service Revenues. Later, the credit balance in Service Revenues will be transferred to the owner’s capital account.

The transaction in the general journal form is:

If a balance sheet is prepared at this time, we must include the balance from the Service Revenues account (as well as the balances from all income statement accounts) in the owner’s capital account.

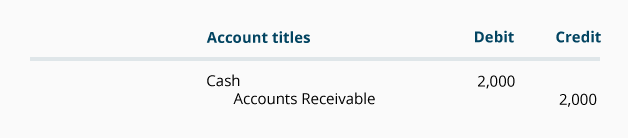

The business collects the $2,000 from the customer who received services 10 days earlier

When the business collects the $2,000 from the customer who had been serviced earlier, the business asset account Cash increases by $2,000 and the business asset account Accounts Receivable decreases by $2,000. Since the transaction has one asset increasing and one asset decreasing by the same amount, there will be no change in the cumulative totals for the accounting equation.

Since assets are on the left side of the accounting equation, both the Cash account and the Accounts Receivable account are expected to have debit balances. Therefore, the Cash account is increased with a debit entry of $2,000; and the Accounts Receivable account is decreased with a credit entry of $2,000.

The transaction in the general journal form is:

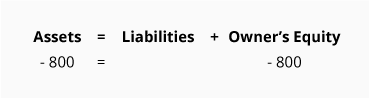

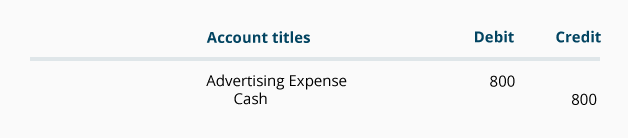

The business incurs $800 of advertising expense and pays the amount immediately

When the business pays the $800, its asset account Cash decreases by $800 and an owner’s equity account decreases by $800. As a result, the change in the accounting equation totals will be:

Since assets are on the left side of the accounting equation, the asset account Cash is expected to have a debit balance. The debit balance will decrease with a credit to Cash for $800.

The other part of the entry will involve the owner’s capital account, which is part of owner’s equity. Since owner’s equity is on the right side of the accounting equation, the owner’s capital account (which is expected to have a credit balance) will decrease with a debit entry of $800. However, instead of recording the debit entry directly in the owner’s capital account, the debit entry will be recorded in the temporary income statement account Advertising Expense. Later, the debit balance in Advertising Expense will be transferred to the owner’s capital account.

The transaction in general journal form is:

If a balance sheet is prepared at this time, the balance in the Advertising Expense account (as well as the balances from all income statement accounts) must be included in the owner’s capital account.

Please let us know how we can improve this explanation

No Thanks

Close

Examples of Debits and Credits in a Corporation

Let’s now reinforce our debit and credit understanding by using five similar examples for a corporation.

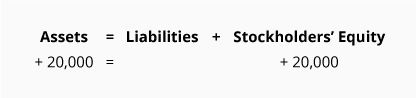

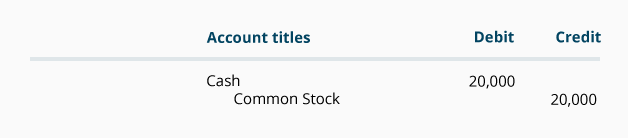

A corporation issues common stock and receives $20,000 of cash

When a corporation issues shares of its no par, no stated value Common Stock to investors for their $20,000 of cash, the corporation’s assets increase by $20,000 and its stockholders’ equity increases by $20,000. As a result, the accounting equation will be in balance:

Since assets are on the left side of the accounting equation, the asset account Cash is expected to have a debit balance and it will increase with a debit entry to Cash for $20,000.

The other part of the entry involves a stockholders’ equity account (Common Stock). Since stockholders’ equity is on the right side of the accounting equation, the Common Stock account is expected to have a credit balance and will increase with a credit entry of $20,000.

The transaction in the general journal form is:

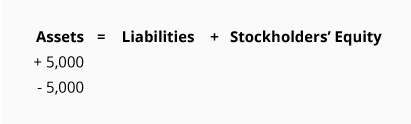

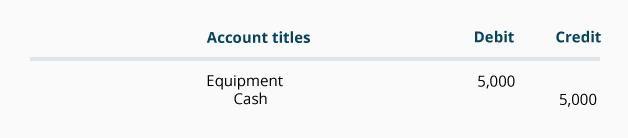

The corporation purchases equipment for $5,000

When the corporation pays $5,000 of its cash for new equipment, the business asset Cash decreases by $5,000 and the business asset account Equipment increases by $5,000. The following shows that the transaction is in balance and that the accounting equation totals and the balance sheet totals should continue to be in balance:

Note: In this topic we show only the change in the accounting equation. To see the cumulative amounts for multiple transactions, visit our Accounting Equation Explanation.

Since assets are on the left side of the accounting equation, the asset account Equipment is expected to have a debit balance. The debit balance in the Equipment account will increase with a debit entry to Equipment for $5,000.

The other part of the entry involves the asset account Cash, which is also expected to have a debit balance. Since the Cash account is decreasing by $5,000, the Cash account must be credited for $5,000.

The transaction in the general journal format is:

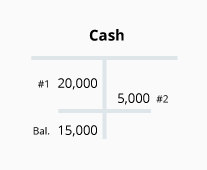

The following T-account illustrates how the debit and credit amounts from the first two transactions have affected the Cash account:

Since Cash is an asset account, its normal or expected balance is a debit balance. Therefore, the Cash account is debited to increase its balance. In the first transaction, we assumed that the corporation was started by investors providing $20,000 of cash for new shares of the corporation’s common stock. This is shown as #1 in the above T-account.

In the second transaction, the corporation spent $5,000 of its cash to purchase equipment. Hence, item #2 had to be a credit to Cash for $5,000 in order to reduce the Cash account balance from $20,000 down to $15,000.

Note that the T-account is usually a sketch the accountant or bookkeeper makes in order to visualize the effects that a transaction will have on the two or more accounts involved in a transaction. (The account appearing in the company’s general ledger will NOT be in the form of a “T” as we have shown it.)

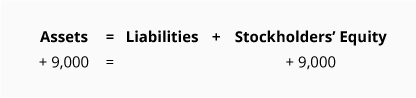

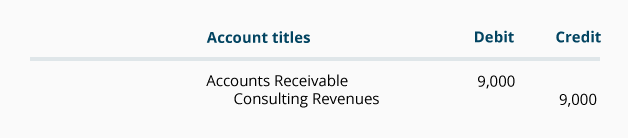

The corporation earns consulting revenues of $9,000 and allows the client to pay 10 days later

When the corporation earns $9,000 by providing a client with consulting services, the corporation’s assets increase by $9,000 and stockholders’ equity increases by $9,000. As a result, the change in the accounting equation will be:

Since assets are on the left side of the accounting equation, the asset account Accounts Receivable is expected to have a debit balance. The debit balance in Accounts Receivable will increase with a debit to Accounts Receivable for $9,000.

The other part of the entry will involve the stockholders’ equity account Retained Earnings. Since stockholders’ equity is on the right side of the accounting equation, the Retained Earnings account (which is expected to have a credit balance) will increase with a credit entry of $9,000. However, instead of recording the credit entry of $9,000 directly to the Retained Earnings account, the credit entry of $9,000 will be recorded in the temporary income statement account entitled Consulting Revenues. Later, the credit balance in Consulting Revenues will be transferred to the Retained Earnings account.

The transaction in the general journal form is:

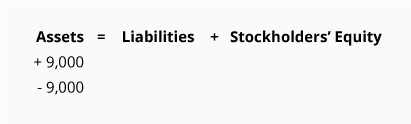

If a balance sheet is prepared at this time, the balance in the account Consulting Revenues (and the balances from all income statement accounts) must be included in Retained Earnings.

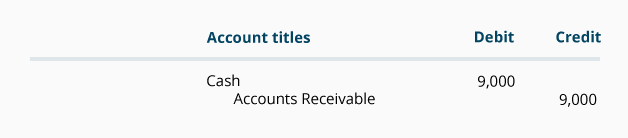

The corporation collects the $9,000 from the client who received services 10 days earlier

When the business collects the $9,000 from the client who had received the consulting services earlier, the corporation’s asset account Cash increases by $9,000 and its asset account Accounts Receivable decreases by $9,000. Since the transaction has one asset account increasing and one asset account decreasing by the same amount there will be no change in the cumulative totals for the accounting equation.

Since assets are on the left side of the accounting equation, both the Cash account and the Accounts Receivable account are expected to have debit balances. Therefore, the Cash account is increased with a debit entry of $9,000; and the Accounts Receivable account is decreased with a credit entry of $9,000.

The transaction in the general journal form is:

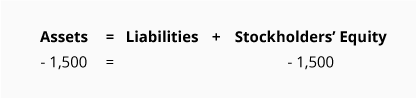

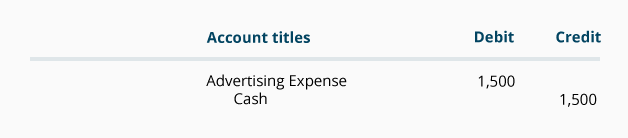

The corporation incurs $1,500 of advertising expense which is paid immediately

When the corporation pays the $1,500 for advertising, its assets decrease by $1,500 and its stockholders’ equity decreases by $1,500. As a result, the change in the accounting equation totals will be:

Since assets are on the left side of the accounting equation, the asset account Cash is expected to have a debit balance. The debit balance will decrease with a credit to Cash for $1,500.

The other part of the entry involves the stockholders’ equity account Retained Earnings. Since stockholders’ equity is on the right side of the accounting equation, the Retained Earnings account’s credit balance is decreased with a debit entry of $1,500. However, instead of recording a debit entry directly in the Retained Earnings account at this time, the debit entry will be recorded in the temporary income statement account Advertising Expense. Later, the debit balance in Advertising Expense will be transferred to the Retained Earnings account.

The transaction in general journal form is:

If a balance sheet is prepared at this time, the balance in the account Advertising Expense (and all balances from the income statement accounts) must be included in Retained Earnings.

Where to Go From Here

We recommend taking our Practice Quiz next, and then continuing with the rest of our Debits and Credits materials (see the full outline below).

We also recommend joining PRO to unlock our premium materials (certificates of achievement, video training, flashcards, visual tutorials, quick tests, quick tests with coaching, cheat sheets, guides, puzzles, business forms, printable PDF files, progress tracking, badges, points, medal rankings, activity streaks, public profile pages, and more).

You should consider our materials to be an introduction to selected accounting and bookkeeping topics, and realize that some complexities (including differences between financial statement reporting and income tax reporting) are not presented. Therefore, always consult with accounting and tax professionals for assistance with your specific circumstances.

The 500 year-old accounting system where every transaction is recorded into at least two accounts. To learn more, see Explanation of Debits and Credits.

A record in the general ledger that is used to collect and store similar information. For example, a company will have a Cash account in which every transaction involving cash is recorded. A company selling merchandise on credit will record these sales in a Sales account and in an Accounts Receivable account.

That part of the accounting system which contains the balance sheet and income statement accounts used for recording transactions.

An account in the general ledger, such as Cash, Accounts Payable, Sales, Advertising Expense, etc. To learn more, see Explanation of Chart of Accounts.

A visual aid used by accountants to illustrate a journal entry’s effect on the general ledger accounts. Debit amounts are entered on the left side of the “T” and credit amounts are entered on the right side.

For the past 52 years, Harold Averkamp (CPA, MBA) has

worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. He is the sole author of all the materials on AccountingCoach.com.