Multiple-Step Income Statement Definition

A multiple-step income statement presents two important subtotals before arriving at a company’s net income. For a company that sells goods (merchandise, products) the first subtotal is the amount of gross profit. The second subtotal is the amount of operating income.

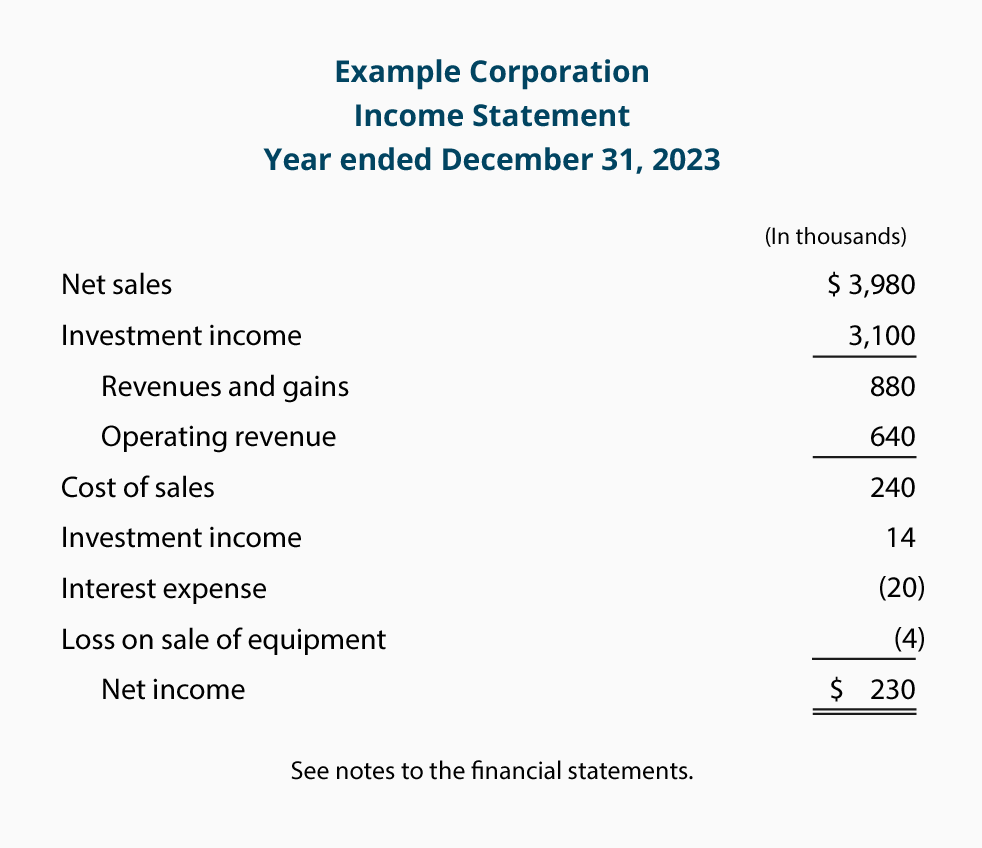

Example of a Multiple-Step Income Statement

Here is an example of a condensed multiple-step income statement for a hypothetical sole proprietorship:

Notice these items on the multiple-step income statement:

- Operating revenues (net sales, service revenues, etc.) and operating expenses (cost of sales, SG&A expenses) appear first

- The subtotal Gross profit is the result of subtracting the Cost of sales from the Net sales

- The subtotal Operating income is the result of subtracting SG&A exp. from the Gross profit

- The nonoperating revenues and expenses and the gains and losses are added/subtracted from the operating income

The important subtotals on the multiple-step income statement are convenient for the reader/user of the income statement.

Multiple-Step vs Single-Step

An alternative income statement format that presents the operating revenues, nonoperating revenues, and gains at the beginning of the income statement, followed by the operating expenses, nonoperating expenses, and losses is the single-step income statement.