Introduction

The common rules that apply to the financial statements distributed by a U.S. company to external users are referred to as accounting principles, generally accepted accounting principles, GAAP (pronounced gap), or US GAAP. These rules or standards allow lenders, investors, and others to make comparisons between companies’ financial statements.

Since 1973, US GAAP has been developed and maintained by the Financial Accounting Standards Board (FASB), a non-government, not-for-profit organization. In 2009, the FASB launched the Accounting Standards Codification (ASC or Codification), which it continues to update. This electronic database contains the official accounting standards (the equivalent of many thousands of printed pages) which apply to the financial reporting of U.S companies and not-for-profit organizations.

[There is also an International Accounting Standards Board (IASB) that issues International Financial Reporting Standards (IFRS) which we will not be discussing.]

In addition to GAAP, U.S. corporations with capital stock trading on a stock exchange must also comply with the regulations of the Securities and Exchange Commission (SEC) and the Internal Revenue Service (IRS), both of which are U.S. government agencies.

WATCH NOW

Advance Your Career with Our PRO Training

In this explanation we begin with brief descriptions of many of the underlying principles, assumptions, concepts, and qualities upon which the complex and detailed accounting standards are based. Examples include historical cost, revenue recognition, full disclosure, materiality, and consistency.

We then review the effect of those underlying principles and concepts on a company’s financial statements such as:

Underlying Accounting Principles, Assumptions, etc.

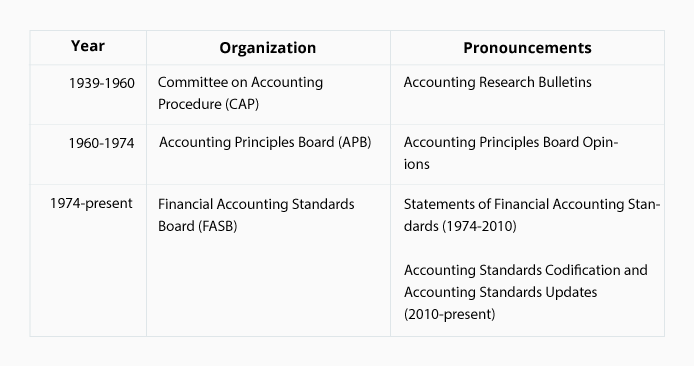

The following chart shows an overview of the accounting profession’s efforts in developing U.S. generally accepted accounting principles (GAAP or US GAAP):

Some of the accounting principles in the Accounting Research Bulletins remain in effect today and are included in the Accounting Standards Codification. However, due to the complexities and sophistication of today’s global business activities and financing, GAAP has become more extensive and more detailed.

Our focus is on the basic, fundamental principles and concepts and what they mean for a business’s financial statements.

We begin with brief descriptions of many of the underlying principles, assumptions, concepts, constraints, qualitative characteristics, etc.

Economic entity assumption

The economic entity assumption allows the accountant to keep the business transactions of a sole proprietorship separate from the sole proprietor’s personal transactions.

It also means that financial statements can be prepared for a group of separate legal corporations that are controlled by one corporation. This group of commonly owned corporations is referred to as the economic entity. The set of financial statements that reports the combined activity of the group is referred to as consolidated financial statements.

Monetary unit assumption

For U.S. companies, the monetary unit assumption allows accountants to express a company’s wide-ranging assets as dollar amounts. Further, it is assumed that the U.S. dollar does not lose its purchasing power over time. Because of this, the accountant combines the $10,000 spent on land in 1980 with the $300,000 spent on a similar adjacent parcel of land in 2025. The result is that the company’s balance sheet will report the combined cost of two parcels at $310,000.

Going concern assumption

The going concern assumption means the accountant believes that the company will not be liquidated in the foreseeable future. In other words, the company will be able to continue operating long enough to meet its obligations and commitments. As a result, the accountant can continue to report most assets at their historical cost and can defer some costs to future periods.

If the company is not considered to be a going concern (meaning the company will not be able to continue in business), it must be disclosed, and liquidation values become the relevant amounts.

Time period (or periodicity) assumption

Accountants assume that a company’s ongoing complex business operations and financial results can be divided into distinct time periods such as months, quarters, and years.

To report a company’s net income for each month, the company will prepare adjusting entries to record each month’s share of depreciation expense, property taxes, insurance, etc. It will also prepare adjusting entries for expenses that occurred but were not paid. Examples include repairs, interest, utilities, etc.

Cost principle

The cost principle (historical cost principle) means the accountant will record transactions at the cash (or equivalent) amount at the time of the transaction. As a result, a company’s most valuable assets are not recorded or reported. Examples include a company’s trademarks, talented team of researchers, unique website domain names, search engine rankings, etc.

Except for certain marketable investment securities, typically an asset’s recorded cost will not be changed due to inflation or market fluctuations.

Full disclosure principle

The full disclosure principle requires a company to provide sufficient information so that an intelligent user can make an informed decision. As a result of this principle, a company’s financial statements will include many disclosures and schedules in the notes to the financial statements.

Revenue recognition principle

Revenues are to be recognized (reported) on a company’s income statement when they are earned. Therefore, a company will report some revenues on its income statement before a customer pays for the goods or services it has received. In the case of cash sales, revenues will be reported when customers pay for their merchandise. If customers pay in advance, the revenues will be recognized (reported) after the money was received.

For example, if an insurance company receives $12,000 on Dec 28, 2025 to provide insurance protection for the year 2026, the insurance company will report $1,000 of revenue in each of the 12 months in the year 2026.

Matching principle or expense recognition

The ideal way to recognize (report) expenses on the income statement is based on a cause-and-effect relationship. For example, if a company sells 5,000 units of Product X, it should report the cost of the 5,000 units on the same income statement as the sales revenues. It is imperative for the cost of goods sold to be calculated accurately, as it is the largest expense on a merchant’s income statement.

When a cause-and-effect relationship isn’t clear, expenses are reported in the accounting period when the cost is used up. For example, the $120,000 cost of equipment with a 10-year life will be charged to expense at a rate of $1,000 per month.

If neither of the above is logical, expenses are reported in the accounting period that the expenses occur. Examples are advertising expense, research expense, salary expense, repairs and maintenance expense, and many others.

Materiality

The concept of materiality means an accounting principle can be ignored if the amount is insignificant. For instance, large companies usually have a policy of immediately expensing the cost of inexpensive equipment instead of depreciating it over its useful life of perhaps 5 years.

Materiality also allows for a mid-size company to report the amounts on its financial statements to the nearest thousand dollars.

Conservatism

If a company has two acceptable ways to record and/or report a transaction, conservatism directs the accountant to choose the alternative that results in less net income or a smaller asset amount. The accountant should be objective, but when doubt exists, conservatism should be used to break the tie.

Consistency and comparability

Accountants are expected to apply accounting principles, procedures, and practices consistently from period to period. If a change is justified, the change must be disclosed on the financial statements.

Comparability means that the user is able to compare the financial statements of one company to those of another company in the same industry. Comparability is enhanced by requiring the use of generally accepted accounting principles.

Relevance and timeliness

For financial statements to be relevant they should be distributed as soon as possible after the end of the accounting period. In other words, relevance is enhanced by timeliness.

To achieve these characteristics, it is likely that some amounts will need to be estimated.

Objectivity and reliability

Accountants are expected to be objective (unbiased). Many businesses are required to have their financial statements audited to assure the users that the amounts are objective and reliable.

The Effect of Accounting Principles on Financial Statements

Now that you have been introduced to many of the underlying accounting principles and concepts, let’s examine what they mean for a company’s financial reporting.

Distributing a complete set of financial statements

The accounting profession believes that a single financial statement is not sufficient for someone to understand a company’s financial affairs. Therefore, if a company releases its financial statement(s) to someone outside of the company, it should distribute a set of financial statements containing the following:

The balance sheet reports the assets, liabilities, and stockholders’ equity as of the final moment of the accounting period (December 31, June 30, etc.).

The other financial statements report the amounts that occurred throughout the accounting period shown in the heading (year ended December 31, three months ended June 30, etc.).

The notes to the financial statements are referenced on each financial statement to inform the user that the notes are an integral part of each financial statement. The notes are necessary because a company’s business activity cannot be communicated completely by the amounts appearing on the face of the financial statements.

In addition to complying with US GAAP, corporations with capital stock that is traded on a stock exchange must also comply with some additional rules and communication required by the U.S. Securities and Exchange Commission (SEC). Regular U.S. corporations must also comply with federal and state income tax reporting regulations.

Accrual Method of Accounting

To properly (report) revenues and expenses on the income statement, and assets and liabilities on the balance sheet, companies must use the accrual method of accounting (or accrual accounting). The following examples illustrate accrual accounting:

-

Revenues are reported on the income statement when they have been earned. Generally, this means there will also be a related asset reported on the company’s balance sheet, such as cash or accounts receivable. In accounting terminology, the revenues and the related asset are recognized (reported on the financial statements) when the revenues and asset have been earned.

A simple example of revenue recognition occurs when a company completes a service for $5,000 on December 28. On the same day, the company bills the customer $5,000 with credit terms of net 30 days. A month later (on January 29) the company receives the $5,000.

On December 28, the company records a $5,000 increase in its current asset account Accounts Receivable and a $5,000 increase in its income statement account Revenues Earned. On January 29, when the company receives the $5,000, it will increase its cash by $5,000 and will reduce its accounts receivable by $5,000.

-

Expenses are reported (recognized) on the income statement when an expense occurs. The date of the company’s payment to the vendor is not relevant.

To illustrate, assume that a company incurs a $3,000 repair expense on December 26. On December 28, the company receives the vendor’s invoice stating that the bill is to be paid within 15 days. On January 8, the company pays $3,000 to the vendor.

The company must record the $3,000 increase in its expenses and liabilities as of December 26 or 28. When the company pays the vendor $3,000 on January 8, the company will decrease its cash balance and will decrease its liabilities.

In short, the company’s financial statements are more complete when the accrual method is used.

To comply with the accrual method, companies record adjusting entries as of the final day of the accounting period. Adjusting entries make certain that the proper amount of expenses and liabilities, and the proper amount of revenues and assets, are reported on the appropriate period’s financial statements.

Revenues Reported on the Income Statement

Under the accrual method, revenues are reported or recognized on the company’s income statement for the period in which the revenues were earned.

Depending on the transactions, revenues may be earned and reported on a company’s income statements at any of the following times:

- Before receiving the money from customers (sales and services were provided on credit)

- At the time customers pay (cash sales)

- After money is received from customers (some future services were required)

To achieve the accrual method, companies will make the following revenue-related adjusting entries at the end of the accounting period to:

- Accrue revenues (and the related receivables) that were earned, but the company had not yet billed the customer

- Defer revenues (and the related liabilities) for money received from customers, but not yet earned by the company

In 2014, the FASB issued an Accounting Standards Update (ASU) entitled Revenue from Contracts with Customers (Topic 606) which provides extensive guidance for reporting revenues on the income statement.

Expenses Reported on the Income Statement

Under the accrual method, expenses are to be reported (recognized) on the company’s income statement during the accounting period in which the expenses:

-

Were caused by revenues (e.g., matching the cost of goods sold and sales commissions with the related revenues)

-

Expired or were used up (e.g., matching prepaid insurance to the accounting periods in which the prepaid amount had expired; systematically allocating the cost of equipment used in the business to the accounting periods in the equipment’s useful life)

-

Had no future economic benefit that could be measured (e.g., advertising expense, office salaries, research expenses)

To achieve the accrual method, companies will make accrual, deferral, depreciation, and other adjusting entries for expenses at the end of each accounting period.

Note: To learn more about the income statement, visit our Explanation and Quiz for this topic.

Assets Reported on the Balance Sheet

The cost principle (or historical cost principles) means that a company’s assets are recorded at their cost at the time of the transaction. Once recorded, the cost of most assets (some marketable investment securities are an exception) will not be increased because of inflation or increases in market value.

To illustrate, assume that 18 years ago a company purchased a parcel of land for its future use at a cost of $50,000. Today, the market value of the land is $300,000. The company’s current balance sheet will report the land at its cost of $50,000.

A company that sells goods will report its inventory at its cost, not at the sales value.

The cost principle prevents a company from recording and reporting its talented employees as assets. Similarly, a company’s brands and logos that were developed internally and enhanced through advertising expenses cannot be reported as assets.

If an asset’s fair value drops below its book or carrying value, the asset’s book value may have to be decreased and an impairment loss reported on the income statement.

Liabilities Reported on the Balance Sheet

Liabilities are a company’s obligations resulting from a past transaction. Typical liabilities include accounts payable, notes or loans payable, wages payable, interest payable, taxes payable, customer deposits, deferred revenue, and more.

At the end of each accounting period, there will be amounts owed by a company, but the company has not yet been billed or has not yet processed the transaction. A few examples include:

- Interest on loans payable

- Electricity and gas charges

- Wages for hourly paid employees that have been earned but not yet processed

- Repair work that was recently done by a contractor

These obligations and the related expense must be recorded for the financial statements to be complete and to comply with the accrual method of accounting. This is done with accrual-type adjusting entries.

Stockholders’ Equity Reported on the Balance Sheet

Stockholders’ equity or shareholders’ equity is the difference between the amount of a corporation’s assets and liabilities that are reported on the balance sheet. (Owner’s equity is the difference between a sole proprietorship’s assets and liabilities.)

Since most of a company’s assets are reported at cost (or lower), the amount reported as stockholders’ equity is not an indicator of the corporation’s market value. Picture a service business that has developed amazing software that generates huge fees with little expenses and the owners draw out most of the profits. As a result, this service business is extremely valuable but has only a small amount reported on its balance sheet for assets and stockholders’ equity.

Note: To learn more about the balance sheet, visit our Explanation and Quiz for this topic.

Notes to the Financial Statements

The full disclosure principle requires that sufficient financial information be presented so that an intelligent person can make an informed decision. As a result of this principle, it is common to find many pages of notes to the financial statements.

A few examples of the many items disclosed in the notes to the financial statements include:

- Summary of significant accounting policies

- Leases

- Income taxes

- Employee benefit plans

- Stock options

- Commitments and contingencies

Where to Go From Here

We recommend taking our Practice Quiz next, and then continuing with the rest of our Accounting Principles materials (see the full outline below).

We also recommend joining PRO to unlock our premium materials (certificates of achievement, video training, flashcards, visual tutorials, quick tests, quick tests with coaching, cheat sheets, guides, puzzles, business forms, printable PDF files, progress tracking, badges, points, medal rankings, activity streaks, public profile pages, and more).

Disclaimer

You should consider our materials to be an introduction to selected accounting and bookkeeping topics (with complexities likely omitted). We focus on financial statement reporting and do not discuss how that differs from income tax reporting. Therefore, you should always consult with accounting and tax professionals for assistance with your specific circumstances.