Introduction

Adjusting entries are accounting journal entries that convert a company’s accounting records to the accrual basis of accounting. An adjusting journal entry is typically made just prior to issuing a company’s financial statements.

To demonstrate the need for an accounting adjusting entry let’s assume that a company borrowed money from its bank on December 1, 2025 and that the company’s accounting period ends on December 31. The bank loan specifies that the first interest payment on the loan will be due on March 1, 2026. This means that the company’s accounting records as of December 31 do not contain any payment to the bank for the interest the company incurred from December 1 through December 31. (Of course the loan is costing the company interest expense every day, but the actual payment for the interest will not occur until March 1.)

For the company’s December income statement to accurately report the company’s profitability, it must include all of the company’s December expenses—not just the expenses that were paid. Similarly, for the company’s balance sheet on December 31 to be accurate, it must report a liability for the interest owed as of the balance sheet date. An adjusting entry is needed so that December’s interest expense is included on December’s income statement and the interest due as of December 31 is included on the December 31 balance sheet. The adjusting entry will debit Interest Expense and credit Interest Payable for the amount of interest from December 1 to December 31.

Another situation requiring an adjusting journal entry arises when an amount has already been recorded in the company’s accounting records, but the amount is for more than the current accounting period. To illustrate let’s assume that on December 1, 2025 the company paid its insurance agent $2,400 for insurance protection during the period of December 1, 2025 through May 31, 2026. The $2,400 transaction was recorded in the accounting records on December 1, but the amount represents six months of coverage and expense. By December 31, one month of the insurance coverage and cost have been used up or expired. Hence the income statement for December should report just one month of insurance cost of $400 ($2,400 divided by 6 months) in the account Insurance Expense. The balance sheet dated December 31 should report the cost of five months of the insurance coverage that has not yet been used up. (The cost not used up is referred to as the asset Prepaid Insurance. The cost that is used up is referred to as the expired cost Insurance Expense.) This means that the balance sheet dated December 31 should report five months of insurance cost or $2,000 ($400 per month times 5 months) in the asset account Prepaid Insurance. Since it is unlikely that the $2,400 transaction on December 1 was recorded this way, an adjusting entry will be needed at December 31, 2025 to get the income statement and balance sheet to report this accurately.

The two examples of adjusting entries have focused on expenses, but adjusting entries also involve revenues. This will be discussed later when we prepare adjusting journal entries.

For now we want to highlight some important points.

There are two scenarios where adjusting journal entries are needed before the financial statements are issued:

- Nothing has been entered in the accounting records for certain expenses or revenues, but those expenses and/or revenues did occur and must be included in the current period’s income statement and balance sheet.

- Something has already been entered in the accounting records, but the amount needs to be divided up between two or more accounting periods.

Each adjusting entry will include:

WATCH NOW

Advance Your Career with Our PRO Training

Adjusting Entries – Asset Accounts

Adjusting entries assure that both the balance sheet and the income statement are up-to-date on the accrual basis of accounting. A reasonable way to begin the process is by reviewing the amount or balance shown in each of the balance sheet accounts. We will use the following preliminary balance sheet, which reports the account balances prior to any adjusting entries:

Let’s begin with the asset accounts:

Cash $1,800

The Cash account has a preliminary balance of $1,800—the amount in the general ledger. Before issuing the balance sheet, one must ask, “Is $1,800 the true amount of cash? Does it agree to the amount computed on the bank reconciliation?” The accountant found that $1,800 was indeed the true balance. (If the preliminary balance in Cash does not agree to the bank reconciliation, entries are usually needed. For example, if the bank statement included a service charge and a check printing charge—and they were not yet entered into the company’s accounting records—those amounts must be entered into the Cash account. Visit our Bank Reconciliation Explanation for a thorough discussion and illustration of the likely journal entries.)

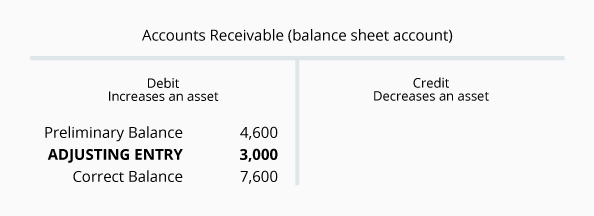

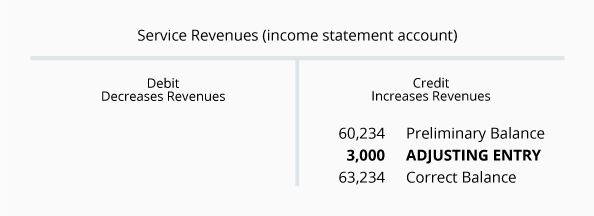

Accounts Receivable $4,600

To determine if the balance in this account is accurate the accountant might review the detailed listing of customers who have not paid their invoices for goods or services. (This is often referred to as the amount of open or unpaid sales invoices and is often found in the accounts receivable subsidiary ledger.) When those open invoices are sorted according to the date of the sale, the company can tell how old the receivables are. Such a report is referred to as an aging of accounts receivable. Let’s assume the review indicates that the preliminary balance in Accounts Receivable of $4,600 is accurate as far as the amounts that have been billed and not yet paid.

However, under the accrual basis of accounting, the balance sheet must report all the amounts the company has an absolute right to receive—not just the amounts that have been billed on a sales invoice. Similarly, the income statement should report all revenues that have been earned—not just the revenues that have been billed. After further review, it is learned that $3,000 of work has been performed (and therefore has been earned) as of December 31 but won’t be billed until January 10. Because this $3,000 was earned in December, it must be entered and reported on the financial statements for December. An adjusting entry dated December 31 is prepared in order to get this information onto the December financial statements.

To assist you in understanding adjusting journal entries, double entry, and debits and credits, each example of an adjusting entry will be illustrated with a T-account.

Here is the process we will follow:

- Draw two T-accounts. (Every journal entry involves at least two accounts. One account to be debited and one account to be credited.)

- Indicate the account titles on each of the T-accounts. (Remember that almost always one of the accounts is a balance sheet account and one will be an income statement account. In a smaller font size we will indicate the type of account next to the account title and we will also indicate some tips about debits and credits within the T-accounts.)

- Enter the preliminary balance in each of the T-accounts.

- Determine what the ending balance ought to be for the balance sheet account.

- Make an adjustment so that the ending amount in the balance sheet account is correct.

- Enter the same adjustment amount into the related income statement account.

- Write the adjusting journal entry.

Let’s follow that process here:

The adjusting entry for Accounts Receivable in general journal format is:

Notice that the ending balance in the asset Accounts Receivable is now $7,600—the correct amount that the company has a right to receive. The income statement account balance has been increased by the $3,000 adjustment amount, because this $3,000 was also earned in the accounting period but had not yet been entered into the Service Revenues account. The balance in Service Revenues will increase during the year as the account is credited whenever a sales invoice is prepared. The balance in Accounts Receivable also increases if the sale was on credit (as opposed to a cash sale). However, Accounts Receivable will decrease whenever a customer pays some of the amount owed to the company. Therefore the balance in Accounts Receivable might be approximately the amount of one month’s sales, if the company allows customers to pay their invoices in 30 days.

At the end of the accounting year, the ending balances in the balance sheet accounts (assets and liabilities) will carry forward to the next accounting year. The ending balances in the income statement accounts (revenues and expenses) are closed after the year’s financial statements are prepared and these accounts will start the next accounting period with zero balances.

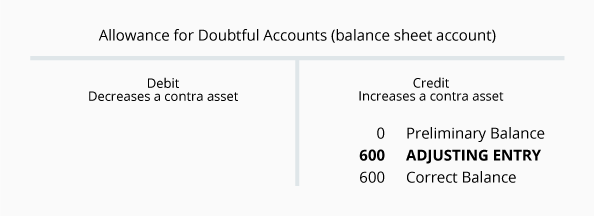

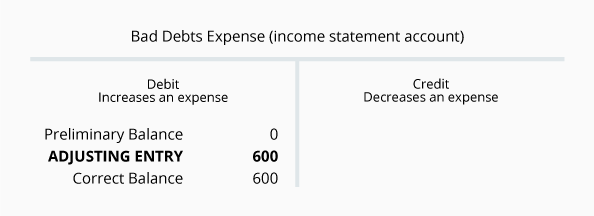

Allowance for Doubtful Accounts $0

(It’s common not to list accounts with $0 balances on balance sheets.)

Although the Allowance for Doubtful Accounts does not appear on the preliminary balance sheet, experienced accountants realize that it is likely that some of the accounts receivable might not be collected. (This could occur because some customers will have unforeseen hardships, some customers might be dishonest, etc.) If some of the $4,600 owed to the company will not be collected, the company’s balance sheet should report less than $4,600 of accounts receivable. However, rather than reducing the balance in Accounts Receivable by means of a credit amount, the credit amount will be reported in Allowance for Doubtful Accounts. (The combination of the debit balance in Accounts Receivable and the credit balance in Allowance for Doubtful Accounts is referred to as the net realizable value.)

Let’s assume that a review of the accounts receivables indicates that approximately $600 of the receivables will not be collectible. This means that the balance in Allowance for Doubtful Accounts should be reported as a $600 credit balance instead of the preliminary balance of $0. The two accounts involved will be the balance sheet account Allowance for Doubtful Accounts and the income statement account Bad Debts Expense.

The adjusting journal entry for Allowance for Doubtful Accounts is:

It is possible for one or both of the accounts to have preliminary balances. However, the balances are likely to be different from one another. Because Allowance for Doubtful Accounts is a balance sheet account, its ending balance will carry forward to the next accounting year. Because Bad Debts Expense is an income statement account, its balance will not carry forward to the next year. Bad Debts Expense will start the next accounting year with a zero balance.

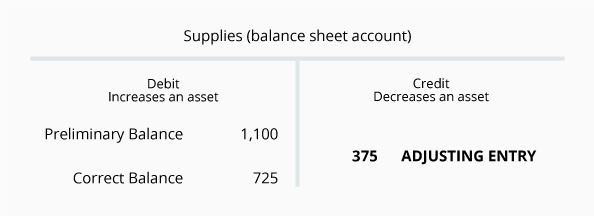

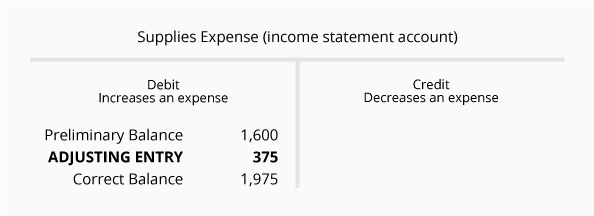

Supplies $1,100

The Supplies account has a preliminary balance of $1,100. However, a count of the supplies actually on hand indicates that the true amount of supplies is $725. This means that the preliminary balance is too high by $375 ($1,100 minus $725). A credit of $375 will need to be entered into the asset account in order to reduce the balance from $1,100 to $725. The related income statement account is Supplies Expense.

The adjusting entry for Supplies in general journal format is:

Notice that the ending balance in the asset Supplies is now $725—the correct amount of supplies that the company actually has on hand. The income statement account Supplies Expense has been increased by the $375 adjusting entry. It is assumed that the decrease in the supplies on hand means that the supplies have been used during the current accounting period. The balance in Supplies Expense will increase during the year as the account is debited. Supplies Expense will start the next accounting year with a zero balance. The balance in the asset Supplies at the end of the accounting year will carry over to the next accounting year.

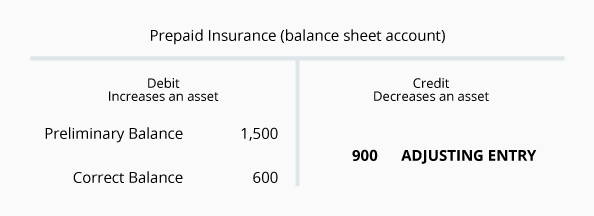

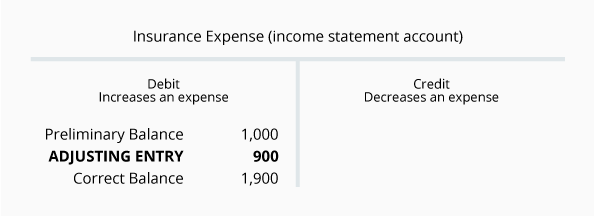

Prepaid Insurance $1,500

The $1,500 balance in the asset account Prepaid Insurance is the preliminary balance. The correct balance needs to be determined. The correct amount is the amount that has been paid by the company for insurance coverage that will expire after the balance sheet date. If a review of the payments for insurance shows that $600 of the insurance payments is for insurance that will expire after the balance sheet date, then the balance in Prepaid Insurance should be $600. All other amounts should be charged to Insurance Expense.

The adjusting journal entry for Prepaid Insurance is:

Note that the ending balance in the asset Prepaid Insurance is now $600—the correct amount of insurance that has been paid in advance. The income statement account Insurance Expense has been increased by the $900 adjusting entry. It is assumed that the decrease in the amount prepaid was the amount being used or expiring during the current accounting period. The balance in Insurance Expense starts with a zero balance each year and increases during the year as the account is debited. The balance at the end of the accounting year in the asset Prepaid Insurance will carry over to the next accounting year.

Equipment $25,000

Equipment is a long-term asset that will not last indefinitely. The cost of equipment is recorded in the account Equipment. The $25,000 balance in Equipment is accurate, so no entry is needed in this account. As an asset account, the debit balance of $25,000 will carry over to the next accounting year.

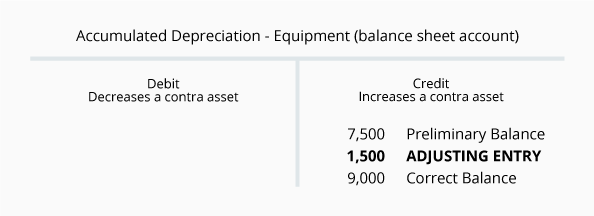

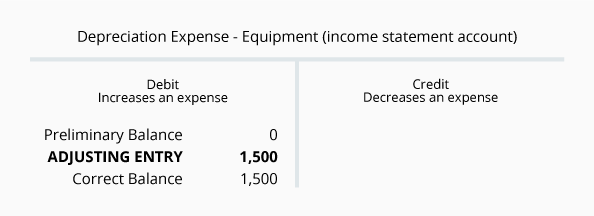

Accumulated Depreciation – Equipment $7,500

Accumulated Depreciation – Equipment is a contra asset account and its preliminary balance of $7,500 is the amount of depreciation actually entered into the account since the Equipment was acquired. The correct balance should be the cumulative amount of depreciation from the time that the equipment was acquired through the date of the balance sheet. A review indicates that as of December 31 the accumulated amount of depreciation should be $9,000. Therefore the account Accumulated Depreciation – Equipment will need to have an ending balance of $9,000. This will require an additional $1,500 credit to this account. The income statement account that is pertinent to this adjusting entry and which will be debited for $1,500 is Depreciation Expense – Equipment.

The adjusting entry for Accumulated Depreciation in general journal format is:

The ending balance in the contra asset account Accumulated Depreciation – Equipment at the end of the accounting year will carry forward to the next accounting year. The ending balance in Depreciation Expense – Equipment will be closed at the end of the current accounting period and this account will begin the next accounting year with a balance of $0.

Adjusting Entries – Liability Accounts

Notes Payable $5,000

Notes Payable is a liability account that reports the amount of principal owed as of the balance sheet date. (Any interest incurred but not yet paid as of the balance sheet date is reported in a separate liability account Interest Payable.) The accountant has verified that the amount of principal actually owed is the same as the amount appearing on the preliminary balance sheet. Therefore, no entry is needed for this account.

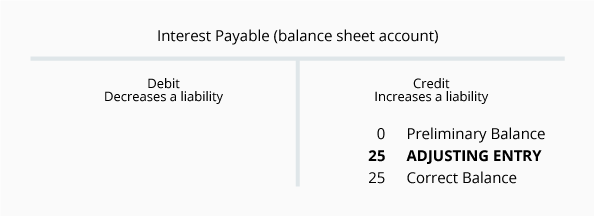

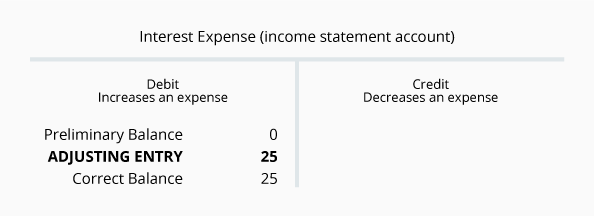

Interest Payable $0

(It’s common not to list accounts with $0 balances on balance sheets.)

Interest Payable is a liability account that reports the amount of interest the company owes as of the balance sheet date. Accountants realize that if a company has a balance in Notes Payable, the company should be reporting some amount in Interest Expense and in Interest Payable. The reason is that each day that the company owes money it is incurring interest expense and an obligation to pay the interest. Unless the interest is paid up to date, the company will always owe some interest to the lender.

Let’s assume that the company borrowed the $5,000 on December 1 and agrees to make the first interest payment on March 1. If the loan specifies an annual interest rate of 6%, the loan will cost the company interest of $300 per year or $25 per month. On March 1 the company will be required to pay $75 of interest. On the December income statement the company must report one month of interest expense of $25. On the December 31 balance sheet the company must report that it owes $25 as of December 31 for interest.

The adjusting journal entry for Interest Payable is:

It is unusual that the amount shown for each of these accounts is the same. In the future months the amounts will be different. Interest Expense will be closed automatically at the end of each accounting year and will start the next accounting year with a $0 balance.

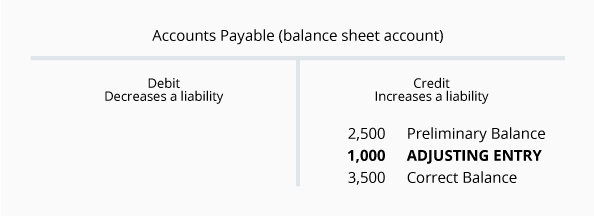

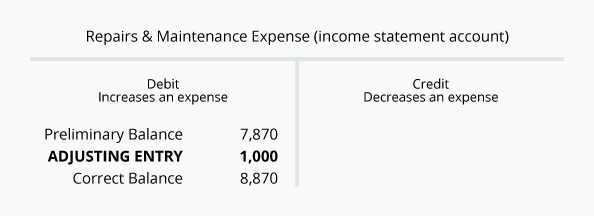

Accounts Payable $2,500

Accounts Payable is a liability account that reports the amounts owed to suppliers or vendors as of the balance sheet date. Amounts are routinely entered into this account after a company has received and verified all of the following: (1) an invoice from the supplier, (2) goods or services have been received, and (3) compared the amounts to the company’s purchase order. A review of the details confirms that this account’s balance of $2,500 is accurate as far as invoices received from vendors.

However, under the accrual basis of accounting the balance sheet must report all the amounts owed by the company—not just the amounts that have been entered into the accounting system from vendor invoices. Similarly, the income statement must report all expenses that have been incurred—not merely the expenses that have been entered from a vendor’s invoice. To illustrate this, assume that a company had $1,000 of plumbing repairs done in late December, but the company has not yet received an invoice from the plumber. The company will have to make an adjusting entry to record the expense and the liability on the December financial statements. The adjusting entry will involve the following accounts:

The adjusting entry for Accounts Payable in general journal format is:

The balance in the liability account Accounts Payable at the end of the year will carry forward to the next accounting year. The balance in Repairs & Maintenance Expense at the end of the accounting year will be closed and the next accounting year will begin with $0.

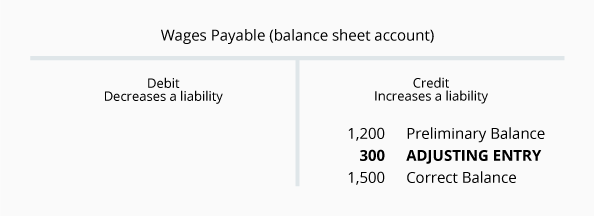

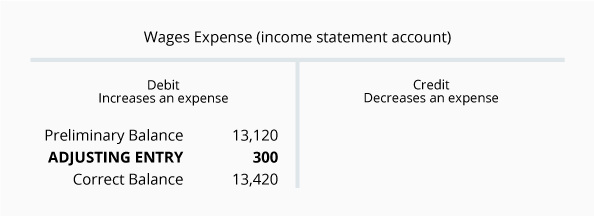

Wages Payable $1,200

Wages Payable is a liability account that reports the amounts owed to employees as of the balance sheet date. Amounts are routinely entered into this account when the company’s payroll records are processed. A review of the details confirms that this account’s balance of $1,200 is accurate as far as the payrolls that have been processed.

However, under the accrual basis of accounting the balance sheet must report all of the payroll amounts owed by the company—not just the amounts that have been processed. Similarly, the income statement must report all of the payroll expenses that have been incurred—not merely the expenses from the routine payroll processing. For example, assume that December 30 is a Sunday and the first day of the payroll period. The wages earned by the employees on December 30-31 will be included in the payroll processing for the week of December 30 through January 5. However, the December income statement and the December 31 balance sheet need to include the wages for December 30-31, but not the wages for January 1-5. If the wages for December 30-31 amount to $300, the following adjusting entry is required as of December 31:

The adjusting journal entry for Wages Payable is:

The $1,500 balance in Wages Payable is the true amount not yet paid to employees for their work through December 31. The $13,420 of Wages Expense is the total of the wages used by the company through December 31. The Wages Payable amount will be carried forward to the next accounting year. The Wages Expense amount will be zeroed out so that the next accounting year begins with a $0 balance.

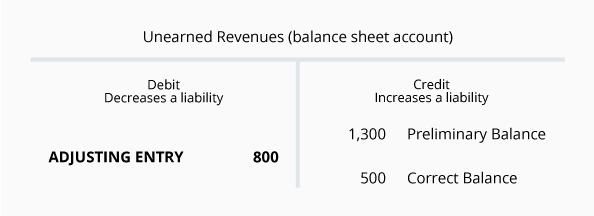

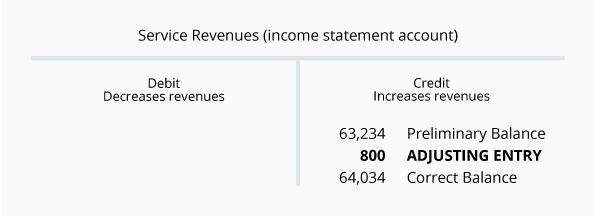

Unearned Revenues $1,300

Unearned Revenues is a liability account that reports the amounts received by a company but have not yet been earned by the company. For example, if a company required a customer with a poor credit rating to pay $1,300 before beginning any work, the company increases its asset Cash by $1,300 and it should increase its liability Unearned Revenues by $1,300.

As the company does the work, it will reduce the Unearned Revenues account balance and increase its Service Revenues account balance by the amount earned (work performed). A review of the balance in Unearned Revenues reveals that the company did indeed receive $1,300 from a customer earlier in December. However, during the month the company provided the customer with $800 of services. Therefore, at December 31 the amount of services due to the customer is $500.

Let’s visualize this situation with the following T-accounts:

The adjusting entry for Unearned Revenues in general journal format is:

Since Unearned Revenues is a balance sheet account, its balance at the end of the accounting year will carry over to the next accounting year. On the other hand Service Revenues is an income statement account and its balance will be closed when the current year is over. Revenues and expenses always start the next accounting year with $0.

Accruals & Deferrals

Adjusting entries are often sorted into two groups: accruals and deferrals.

Accruals

Accruals (or accrual-type adjusting entries) involve both expenses and revenues and are associated with the first scenario mentioned in the introduction to this topic:

- Nothing has been entered in the accounting records for certain expenses and/or revenues, but those expenses and/or revenues did occur and must be included in the current period’s income statement and balance sheet.

Accrual of Expenses

An accountant might say, “We need to accrue the interest expense on the bank loan.” That statement is made because nothing had been recorded in the accounts for interest expense, but the company did indeed incur interest expense during the accounting period. Further, the company has a liability or obligation for the unpaid interest up to the end of the accounting period. What the accountant is saying is that an accrual-type adjusting journal entry needs to be recorded.

The accountant might also say, “We need to accrue for the wages earned by the employees on Sunday, December 30, and Monday, December 31.” This means that an accrual-type adjusting entry is needed because the company incurred wages expenses on December 30-31 but nothing will be entered routinely into the accounting records by the end of the accounting period on December 31.

A third example is the accrual of utilities expense. Utilities provide the service (gas, electric, telephone) and then bill for the service they provided based on some type of metering. As a result the company will incur the utility expense before it receives a bill and before the accounting period ends. Hence, an accrual-type adjusting journal entry must be made in order to properly report the correct amount of utilities expenses on the current period’s income statement and the correct amount of liabilities on the balance sheet.

Accrual of Revenues

Accountants also use the term “accrual” or state that they must “accrue” when discussing revenues that fit the first scenario. For example, an accountant might say, “We need to accrue for the interest the company has earned on its certificate of deposit.” In that situation the company probably did not receive any interest nor did the company record any amounts in its accounts, but the company did indeed earn interest revenue during the accounting period. Further the company has the right to the interest earned and will need to list that as an asset on its balance sheet.

Similarly, the accountant might say, “We need to prepare an accrual-type adjusting entry for the revenues we earned by providing services on December 31, even though they will not be billed until January.”

Deferrals

Deferrals or deferral-type adjusting entries can pertain to both expenses and revenues and refer to the second scenario mentioned in the introduction to this topic:

- Something has already been entered in the accounting records, but the amount needs to be divided up between two or more accounting periods.

Deferral of Expenses

An accountant might say, “We need to defer some of the insurance expense.” That statement is made because the company may have paid on December 1 the entire bill for the insurance coverage for the six-month period of December 1 through May 31. However, as of December 31 only one month of the insurance is used up. Hence the cost of the remaining five months is deferred to the balance sheet account Prepaid Insurance until it is moved to Insurance Expense during the months of January through May. If the company prepares monthly financial statements, a deferral-type adjusting entry may be needed each month in order to move one-sixth of the six-month cost from the asset account Prepaid Insurance to the income statement account Insurance Expense.

The accountant might also say, “We need to defer some of the cost of supplies.” This deferral is necessary because some of the supplies purchased were not used or consumed during the accounting period. An adjusting entry will be necessary to defer to the balance sheet the cost of the supplies not used, and to have only the cost of supplies actually used being reported on the income statement. The costs of the supplies not yet used are reported in the balance sheet account Supplies and the cost of the supplies used during the accounting period are reported in the income statement account Supplies Expense.

Deferral of Revenues

Deferrals also involve revenues. For example if a company receives $600 on December 1 in exchange for providing a monthly service from December 1 through May 31, the accountant should “defer” $500 of the amount to a liability account Unearned Revenues and allow $100 to be recorded as December service revenues. The $500 in Unearned Revenues will be deferred until January through May when it will be moved with a deferral-type adjusting entry from Unearned Revenues to Service Revenues at a rate of $100 per month.

Avoiding Adjusting Entries

If you want to minimize the number of adjusting journal entries, you could arrange for each period’s expenses to be paid in the period in which they occur. For example, you could ask your bank to charge your company’s checking account at the end of each month with the current month’s interest on your company’s loan from the bank. Under this arrangement December’s interest expense will be paid in December, January’s interest expense will be paid in January, etc. You simply record the interest payment and avoid the need for an adjusting entry. Similarly, your insurance company might automatically charge your company’s checking account each month for the insurance expense that applies to just that one month.

Where to Go From Here

We recommend taking our Practice Quiz next, and then continuing with the rest of our Adjusting Entries materials (see the full outline below).

We also recommend joining PRO to unlock our premium materials (certificates of achievement, video training, flashcards, visual tutorials, quick tests, quick tests with coaching, cheat sheets, guides, puzzles, business forms, printable PDF files, progress tracking, badges, points, medal rankings, activity streaks, public profile pages, and more).

Disclaimer

You should consider our materials to be an introduction to selected accounting and bookkeeping topics (with complexities likely omitted). We focus on financial statement reporting and do not discuss how that differs from income tax reporting. Therefore, you should always consult with accounting and tax professionals for assistance with your specific circumstances.

Earn Our Certificate

for This Topic

When you join PRO, you will receive instant access to 16 different Certificates of Achievement plus our Bookkeeping Certificate of Excellence.

View PRO Features